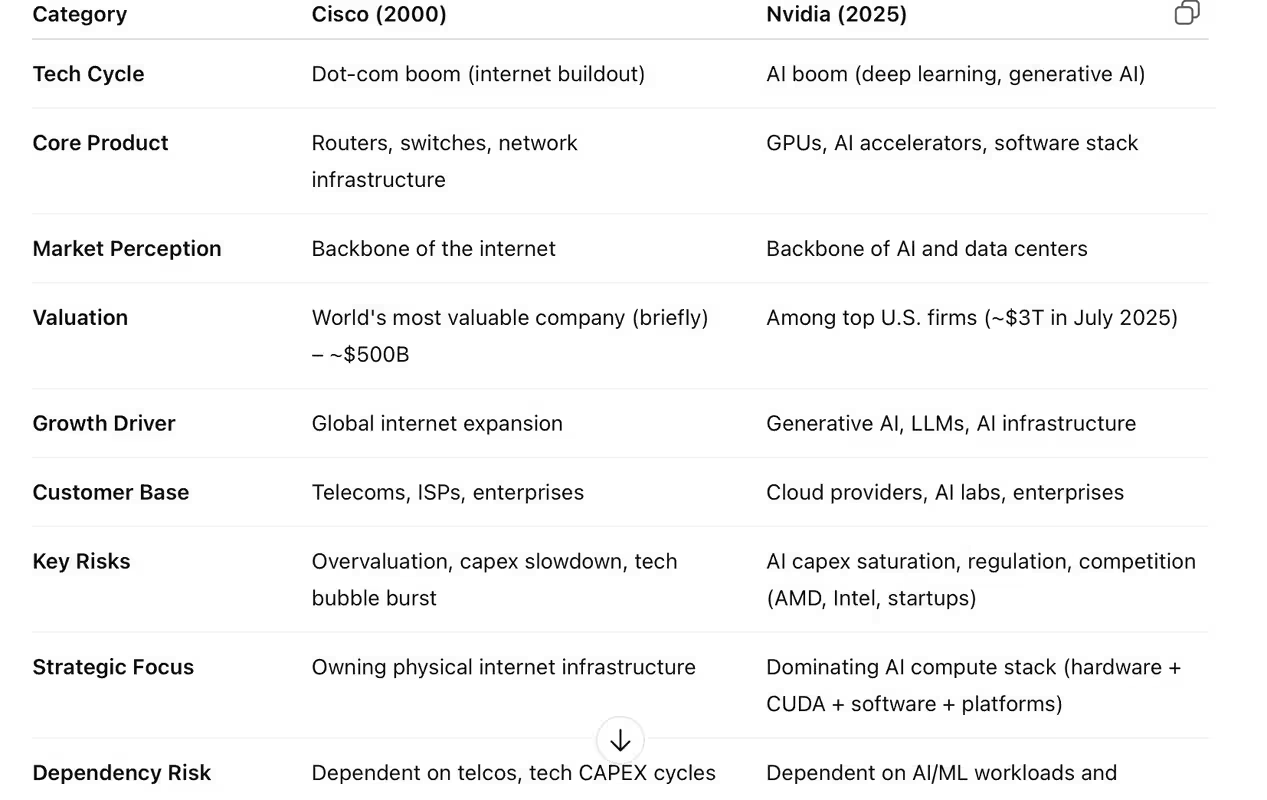

🕰 Cisco in 2000:

Fueled by the internet gold rush.

Every business was getting online; Cisco sold the critical hardware.

Its market cap peaked near $555B in March 2000.

Valuation metrics (like P/E ratio) became stretched.

After the dot-com crash, revenue slowed and the stock collapsed ~80%.

Cisco remained a strong company but stopped being seen as "transformational."

Nvidia in 2025:

Nvidia in 2025:Central to the AI gold rush, especially with LLMs (ChatGPT, Claude, Gemini).

Nvidia chips power everything from cloud AI to robotics to autonomous vehicles.

The company has built a full stack: hardware (GPUs), networking (Mellanox), and software (CUDA, Nvidia AI Enterprise).

Valuation is high (~$3 trillion+), but backed by huge revenue and profit growth.

Risks: over-reliance on hyperscalers, rising competition, AI capex normalization, geopolitical supply chain issues.

Conclusion

ConclusionNvidia in 2025 resembles Cisco in 2000 in that:

Both were/are seen as essential tech enablers of their era.

Each rode a massive macro tech trend (Internet for Cisco, AI for Nvidia).

Each hit massive valuations as a result.

But Nvidia may be more defensible due to:

Stronger margins (software leverage).

Greater vertical integration (hardware + software).

More diverse use cases (beyond just cloud).